- tusemezane@kikwetusacco.com

- +254 704 895 555

- Your reliable Sacco Partner |

- X

Learn how SACCO loan top‑up and refinancing work in Kenya. Access extra funds, lower your payments, or restructure debt. Step‑by‑step guide with requirements.

You have an existing SACCO loan.

Now you need more money. Or you want lower monthly payments.

What are your options?

Two powerful tools can help: loan top‑up and loan refinancing.

Both are available in most Kenyan SACCOs, yet many members don’t understand how they work.

In this guide, you’ll learn:

What a SACCO loan top‑up is (and when to use it)

How refinancing can lower your payments

Requirements, limits, and step‑by‑step processes

Pros, cons, and common mistakes

Whether these options are right for your situation

Let’s start with the basics.

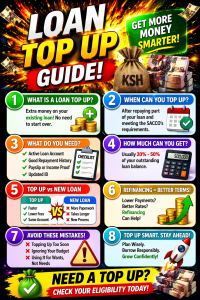

What is a SACCO loan top‑up?

A SACCO loan top‑up allows a borrower to access additional funds on an existing loan after repaying part of it. The new amount is added to the remaining balance, and the repayment term may be extended.

Imagine you borrowed KES 200,000.

You have repaid KES 80,000. Your remaining balance is KES 120,000.

With a top‑up, the SACCO can give you extra money – say KES 50,000.

Your new total balance becomes KES 170,000.

You then repay that amount over a fresh or extended term.

This is faster than applying for a completely new loan.

It uses your existing repayment history.

💡 Kikwetu Pro Tip: A top‑up is not free money. You still pay interest on the total amount. Use it only when you genuinely need extra funds.

Not everyone qualifies immediately.

SACCOs have clear rules.

✅ You have repaid at least 30–50% of your original loan.

✅ Your repayment history is clean (no missed payments).

✅ Your savings record remains active and consistent.

✅ Your debt‑to‑income ratio still allows additional borrowing.

✅ Your CRB status is positive (no defaults).

Some SACCOs also require that you have been a member for a minimum period (e.g., 6 months).

Others may ask for fresh guarantor approvals.

💡 Kikwetu Pro Tip: The best time to request a top‑up is just after you’ve made a significant repayment. Your remaining balance is lower, and your repayment discipline is visible.

Can you top up a SACCO loan?

Yes. Most SACCOs in Kenya allow loan top‑ups once you have repaid a portion of your current loan and meet eligibility requirements, including a clean repayment record and sufficient savings history.

Before applying, gather these items.

| Requirement | Details |

|---|---|

| Loan repayment record | At least 6–12 months of on‑time payments |

| Remaining balance | Must be less than original amount (ideally 50–70% repaid) |

| Savings consistency | No skipped monthly contributions |

| Income proof | Payslips or bank statements (last 3 months) |

| CRB report | Clean or settled status |

| Guarantors | May need 1–2 existing members (depending on top‑up size) |

| Top‑up application form | Available from your SACCO |

Some SACCOs also charge a small processing fee (1–2% of the top‑up amount).

Always ask for the total cost before signing.

The limit depends on your savings and repayment history.

You can usually borrow up to 3 times your total savings (including the existing loan balance).

The top‑up amount itself may be limited to 50–100% of your original loan.

Your new total loan cannot exceed the SACCO’s maximum lending limit (e.g., KES 5 million for most SACCOs).

Example:

You have KES 100,000 in savings.

Your current loan balance is KES 120,000.

The SACCO can lend up to 3 × savings = KES 300,000 total.

Therefore, you could top up by KES 180,000 (new total KES 300,000).

However, each SACCO sets its own formula.

At Kikwetu, we assess each member individually based on savings, repayment behaviour, and income stability.

💡 Kikwetu Pro Tip: A higher top‑up means higher monthly payments. Only take what you truly need.

You have two ways to get extra money: top‑up or a new loan.

Here’s how they compare.

| Feature | Loan Top‑Up | New Loan |

|---|---|---|

| Processing speed | Faster (uses existing file) | Slower (new approval process) |

| Paperwork | Minimal (just top‑up form) | Full application + guarantors |

| Interest rate | Same as original loan | May be different (usually similar) |

| Repayment term | Often extended | Fresh term |

| Impact on savings | No change | May require new savings commitment |

| Best for | Quick extra cash | Larger, separate borrowing |

When to choose a top‑up:

You need funds urgently.

You have a good repayment record.

You don’t want to find new guarantors.

When to choose a new loan:

You want to keep the original loan separate (e.g., different purpose).

Your current loan is almost paid off.

You want a fresh repayment schedule without extending the old debt.

💡 Kikwetu Pro Tip: If your original loan has a very high interest rate, consider refinancing instead (see below). A new loan might offer better terms.

What is SACCO loan refinancing?

Refinancing means replacing your existing loan with a new one, usually with better terms – lower interest, longer repayment period, or lower monthly payments. You can refinance within the same SACCO or transfer from another lender.

✅ Lower monthly payments – extend the term.

✅ Reduce interest rate – if your credit score improved.

✅ Consolidate multiple loans into one.

✅ Switch from flat rate to reducing balance (if your original loan was flat rate).

Refinancing is different from a top‑up.

A top‑up adds money to your existing loan.

Refinancing replaces the entire loan with a new agreement.

Follow these steps to refinance within the same SACCO or from another lender.

Write down:

Remaining balance

Interest rate

Remaining repayment period

Monthly payment amount

Talk to your SACCO about current loan products.

Ask if they offer lower rates for existing members with good history.

Submit a new loan application.

You may need fresh guarantors if the amount is large.

Once approved, the SACCO disburses the funds.

You use that money to clear your original loan (whether at the same SACCO or another institution).

You now have one loan with better terms.

Keep your savings active to maintain eligibility for future benefits.

💡 Kikwetu Pro Tip: If you refinance with the same SACCO, ask them to waive processing fees. Loyalty often comes with perks.

Yes. This is a powerful form of refinancing.

You move your debt from a higher‑cost lender to a cheaper SACCO.

Join Kikwetu (if not already a member).

Build savings for at least 3 months.

Apply for a loan takeover – we pay off your existing loan directly.

Repay Kikwetu at lower interest rates.

This works for:

Bank loans

Microfinance loans

Loans from other SACCOs (with higher rates)

👉 Read our detailed guide: [How to Transfer Your Loan from a Bank to a SACCO]

| Pro | Why It Helps |

|---|---|

| Fast access | No need for a new loan application from scratch |

| Less paperwork | Uses existing guarantors and savings |

| Flexible amounts | Borrow only what you need |

| Builds credit | On‑time repayments improve your profile |

| Keeps savings intact | Your Wealth Vault continues earning interest |

| Con | What to Watch For |

|---|---|

| Longer debt period | Extending the term means paying interest for more months |

| Higher total interest | Adding money increases overall cost |

| Risk of over‑borrowing | Temptation to take more than needed |

| May require new guarantors | If top‑up exceeds original loan, fresh guarantees may be needed |

💡 Kikwetu Pro Tip: Before topping up, calculate the total additional interest. Sometimes a small personal loan (outside the SACCO) is cheaper for short‑term needs.

❌ Topping up just because you can – only borrow for genuine needs.

❌ Ignoring the new repayment amount – use a loan calculator first.

❌ Forgetting about processing fees – they reduce the net amount you receive.

❌ Not checking your CRB – a hidden default can block approval.

❌ Assuming the interest rate stays the same – some SACCOs adjust rates for top‑ups.

❌ Using top‑up for consumption – daily expenses are better managed with a budget, not more debt.

Is loan top‑up risky?

Loan top‑up carries risks if you borrow more than you can repay or extend the term unnecessarily. It can increase total interest paid and prolong debt. However, used wisely, it provides affordable access to extra funds.

✅ Calculate your new monthly payment before accepting.

✅ Ensure your debt‑to‑income ratio stays below 40%.

✅ Avoid topping up repeatedly without repaying.

✅ Use extra funds for productive purposes (business, education, assets).

Yes, if mismanaged.

Every top‑up adds to your outstanding balance.

Over time, you could end up with a loan that never seems to decrease.

Example of a debt spiral:

Borrow KES 100,000, repay KES 20,000, top up KES 30,000 → balance KES 110,000.

Repay another KES 20,000, top up KES 40,000 → balance KES 130,000.

You keep adding without making real progress.

The safe approach:

Only top up when you have repaid at least half of the original loan.

Set a rule: one top‑up per loan, maximum.

Use the extra cash to increase your income (e.g., buy stock for your business).

💡 Kikwetu Pro Tip: If you need frequent top‑ups, consider a credit line or overdraft instead. Some SACCOs offer revolving loans for ongoing needs.

When should you refinance a SACCO loan?

Refinancing is a good idea when interest rates have dropped, your credit score has improved, or you need lower monthly payments to free up cash flow. It may also help consolidate multiple debts.

A SACCO loan top‑up allows a borrower to access additional funds on an existing loan after repaying part of it. The new amount is added to the remaining balance.

Yes. Most Kenyan SACCOs allow top‑ups once you have repaid a portion of your current loan and meet eligibility requirements.

Refinancing can be beneficial if it lowers your monthly payments or improves your repayment terms. However, extending the term may increase total interest paid.

Typically up to 3 times your savings minus your current outstanding balance. Each SACCO has its own formula. At Kikwetu, we assess individually.

Sometimes. If the top‑up amount exceeds the original loan, the SACCO may require fresh guarantors or updated documentation.

Yes. This is called loan transfer or takeover. Kikwetu Sacco can pay off your external loan, and you repay us at lower rates.

A top‑up adds money to your existing loan. Refinancing replaces the entire loan with a new agreement, often with better terms.

Not directly. However, if you miss payments on the increased balance, that default will be reported. Always ensure you can afford the new repayment.

At Kikwetu Sacco, we make loan restructuring simple and affordable.

✅ Low interest rates – 1% per month, reducing balance.

✅ Fast top‑up approvals – often within 2–3 days.

✅ Flexible refinancing – consolidate debt from banks or other SACCOs.

✅ Member‑friendly terms – we work with you, not against you.

✅ Digital access – apply via M‑Pesa or our app.

👉 Whether you need extra cash or want to lower your payments, we’re here to help.

Don’t struggle with high payments or missed opportunities.

Talk to Kikwetu Sacco today.

👉 Apply for a Loan Top‑Up Now

👉 Request Refinancing

👉 Speak to a Loan Officer

Last Updated: April 18, 2026

Reviewed by Kikwetu Sacco Financial Team

This content has been reviewed by the Kikwetu Sacco Financial Team, a group of professionals with experience in SACCO lending, savings management, and financial literacy in Kenya. The review ensures the information is accurate, practical, and aligned with current credit and loan practices.

Join us today and start growing your money the smart way.

Contact Kikwetu Sacco | Contact Nyota Njema

Your funds are safely stored with Kikwetu Sacco.

We prioritize superior service in all our interactions.

Access loans at lower rates than traditional banking institutions.

As part of a shared-goal community, members benefit from collective support.

We emphasize savings discipline, especially for Kenyan youth.

Members can save and borrow to invest in land, up to three times their saved amount.