- tusemezane@kikwetusacco.com

- +254 704 895 555

- Your reliable Sacco Partner |

- X

Refinancing vs top‑up – which saves you more money? Learn the differences, costs, and when to choose each. Kenya examples and expert tips inside.

When you have an existing loan, one big decision can appear.

Should you top up your loan to get extra cash?

Or should you refinance to get better terms?

Both options can improve your finances.

However, choosing the wrong one may cost you thousands of shillings.

In this guide, you’ll learn:

What loan top‑up and refinancing mean

The key differences (with a comparison table)

Which option actually saves you more money

When to choose each (real Kenya examples)

Common mistakes and how to avoid them

A simple decision framework

Let’s start with the basics.

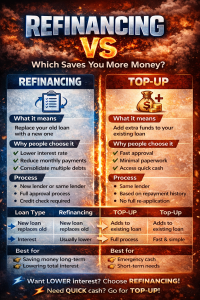

What is a loan top‑up?

A loan top‑up allows you to borrow additional money on top of your existing loan without closing the current one. Your loan balance increases, and you repay the new total over the remaining or extended term.

Imagine you have a current loan of KES 200,000.

You have repaid KES 80,000, so your balance is KES 120,000.

If you need extra KES 100,000, you can apply for a top‑up.

The SACCO adds that amount to your remaining balance.

Your new total becomes KES 220,000.

You then repay this new balance.

Your monthly payment may increase, or your term may be extended.

✅ Key features of a top‑up:

You keep the same loan account.

Approval is usually faster than a new loan.

You get extra funds without starting from scratch.

Interest continues on the higher balance.

💡 Kikwetu Pro Tip: A top‑up is great for urgent needs like school fees or business stock. However, it adds to your debt, so use it wisely.

What is loan refinancing?

Loan refinancing means replacing your current loan with a new loan that has better terms – such as a lower interest rate, longer repayment period, or smaller monthly payments. The old loan is paid off, and you start fresh.

Let’s use the same KES 200,000 loan at 15% interest.

You are struggling with high monthly payments.

You find a SACCO offering 12% interest.

You apply for a refinancing loan of KES 200,000 from that SACCO.

They pay off your old loan directly.

Now you owe the SACCO KES 200,000 at 12%.

Your monthly payments drop.

Your total interest cost decreases.

✅ Key features of refinancing:

Old loan is cleared completely.

New loan has improved terms.

You may get a longer repayment period.

You can also consolidate multiple debts into one.

💡 Kikwetu Pro Tip: Refinancing is ideal when interest rates have fallen or your credit score has improved. It saves you money over the long term.

This table helps you see the differences at a glance.

| Feature | Loan Top‑Up | Loan Refinancing |

|---|---|---|

| Purpose | Get extra cash | Reduce cost or improve terms |

| Loan balance | Increases | Replaced (usually same or lower) |

| Monthly payments | Often higher | Usually lower |

| Total interest cost | Can increase | Can decrease |

| Application process | Faster (uses existing file) | Slightly longer (new approval) |

| Best for | Urgent cash needs | Long‑term savings |

| Effect on debt | Adds more debt | Restructures existing debt |

This table can help you decide at a glance.

However, let’s dig deeper into costs.

Which is better, refinancing or top‑up?

Refinancing is better for reducing monthly payments and total interest. A top‑up is better for accessing additional funds quickly, but it increases your total debt and interest cost.

Short answer: Refinancing saves you more money in most cases.

Why?

Refinancing focuses on lowering your interest rate or extending your term.

That reduces your monthly burden and total repayment.

A top‑up, on the other hand, adds more debt.

Even if the interest rate stays the same, you pay interest on a larger amount for longer.

Example comparison:

Refinancing a KES 200,000 loan from 18% to 12% could save you tens of thousands in interest.

Topping up the same loan by KES 50,000 adds extra interest over the remaining term.

Final rule:

Want to save money long‑term? → Refinance

Need quick extra cash? → Top‑up (but be aware of the cost)

Let’s use a realistic Kenyan scenario.

Current loan:

Amount: KES 200,000

Interest rate: 15% per year (reducing balance)

Remaining term: 12 months

Monthly payment: approx. KES 18,000

You need extra cash for school fees.

You top up by KES 100,000.

New balance: KES 300,000

New monthly payment (same 15%, same remaining term): approx. KES 27,000

Total interest paid over the term increases significantly.

Result: Higher monthly burden, more total interest.

You find a SACCO offering 12% interest.

You refinance the KES 200,000 balance.

New monthly payment (12%, 12 months): approx. KES 17,800

Total interest saved: several thousand shillings.

Result: Lower monthly payment, less total interest.

Conclusion: Refinancing saves you money. Top‑up gives you cash but costs more.

💡 Kikwetu Pro Tip: If you need both – extra cash and lower payments – consider refinancing first to get a better rate, then ask for a small top‑up as part of the new loan. Some SACCOs allow this.

A top‑up is not always bad. It makes sense in these situations.

Emergencies don’t wait.

If you need money quickly for medical bills, urgent repairs, or a time‑sensitive business opportunity, a top‑up is faster than a new loan.

If your interest rate is low (e.g., 10–12%) and your monthly payments are comfortable, adding a top‑up may still be affordable.

Refinancing can take a week or two.

A top‑up often takes 2–3 days.

When time is critical, top‑up wins.

Use the top‑up to buy stock for your business, invest in farming, or pay for training that boosts your earnings.

If the return on investment exceeds the interest cost, it’s a smart move.

💡 Kikwetu Pro Tip: Avoid topping up for luxury spending or daily expenses. That’s how debt spirals start.

Refinancing is usually the smarter financial choice.

Anything above 14–15% annually is expensive.

Refinancing to 12% or lower can save you thousands.

If you struggle to pay every month, refinancing to a longer term lowers your instalment.

This frees up cash flow for other needs.

Refinancing reduces total interest paid.

Over 2–5 years, the savings add up significantly.

If you have several loans (bank, mobile lender, another SACCO), refinancing can combine them into one.

One payment, lower interest, less stress.

If you were listed on CRB but have since cleared your debts, you may now qualify for better rates.

Refinancing rewards your improved financial behaviour.

💡 Kikwetu Pro Tip: Even if you’re happy with your current loan, check rates once a year. You might find a better deal.

Many borrowers make costly errors. Don’t be one of them.

You focus on the cash you receive.

You forget the extra interest you’ll pay.

Always ask: “How much will I repay in total after the top‑up?”

If you have only a few months left on your loan, most interest has already been paid.

Refinancing then saves little.

Best time: At least 12 months before the loan ends.

Refinancing may include processing fees (1–3%), insurance, or legal charges.

Factor these into your comparison.

New phone, expensive holiday, or a big party – these are not good reasons to top up.

You’ll be paying for them long after the fun is gone.

Lenders often have flexible options.

They may offer a better deal to keep your business.

Always ask before going elsewhere.

Use this simple checklist when you’re unsure.

| Your Goal | Recommended Option |

|---|---|

| Need urgent cash (within days) | Top‑up |

| Want lower monthly payments | Refinance |

| Want to save total interest | Refinance |

| Have a high interest rate (>15%) | Refinance |

| Have a low interest rate (<12%) and need cash | Top‑up (cautiously) |

| Want to consolidate multiple debts | Refinance |

| Your income has dropped | Refinance (longer term, lower payments) |

| You have a short‑term cash flow gap | Top‑up (if you can repay quickly) |

💡 Kikwetu Pro Tip: When in doubt, run the numbers. Use a loan calculator or ask your SACCO to show you both scenarios.

Yes. This is an advanced but powerful approach.

Example:

You refinance your existing high‑cost loan to a lower interest rate.

Once the new loan is active, you ask for a small top‑up (since you now have better terms).

This way, you get extra cash and a lower rate.

However, be careful not to over‑borrow.

Only do this if your income can support the new total balance.

💡 Kikwetu Pro Tip: At Kikwetu, we can help you structure a combined solution. Talk to our loan officers.

Yes, it does.

A top‑up increases your loan balance.

Even if your monthly payment stays similar, you’ll be in debt for longer.

If you lose income or face an emergency, the higher balance makes default more likely.

Risk signs:

Topping up repeatedly without significant repayment.

Using top‑ups to pay for daily expenses.

Your debt‑to‑income ratio exceeds 40%.

How to manage risk:

Limit top‑ups to once per loan.

Only top up for productive purposes (business, education, assets).

Keep an emergency fund so you don’t rely on top‑ups.

Yes, when done correctly.

Refinancing lowers your monthly payments.

That improves your cash flow.

You are less likely to miss a payment.

Also, a lower interest rate means more of your payment goes to the principal.

You build equity faster.

However, refinancing to a much longer term (e.g., from 1 year to 5 years) can increase total interest.

Always compare total repayment, not just monthly payment.

A lower monthly payment doesn’t always mean lower total cost.

Ask the lender for the total amount you will repay over the full term.

Don’t accept the first offer.

Ask for:

Lower interest rate

Waived processing fees

Flexible repayment schedule

Just because you qualify for KES 500,000 doesn’t mean you should take it.

Borrow only what you need.

If you sense trouble (e.g., income drop), contact your SACCO before you miss a payment.

They can restructure or refinance to help you.

In Kenya, SACCOs offer some of the most affordable loan products.

They are member‑owned, so their goal is not to maximise profit from you.

What this means for you:

Refinancing within a SACCO is often cheaper than moving to a bank.

Top‑ups are easier to access because the SACCO already knows your history.

Your savings and shares strengthen your bargaining power.

At Kikwetu Sacco, we actively help members restructure debt.

We don’t want you to struggle. We want you to succeed.

Does refinancing save money?

Yes. Refinancing can save money by lowering your interest rate, reducing monthly payments, or shortening the loan term. The savings depend on your current loan terms and the new offer.

Is a loan top‑up expensive?

A loan top‑up can increase your total repayment cost because it adds more debt to your existing loan. Even with the same interest rate, you pay interest on a larger balance for a longer period.

Refinancing is better for reducing monthly payments and total interest. A top‑up is better for accessing additional funds quickly. Your choice depends on your goal.

Yes. Refinancing can save money by lowering interest rates and extending the repayment period, which reduces monthly burden and total interest.

A loan top‑up can increase your total repayment cost because it adds more debt to your existing loan. Use it only for productive needs and repay quickly.

Yes. Some lenders allow you to refinance for a higher amount than your current balance, effectively combining refinancing with a top‑up. Ask your SACCO.

Refinance when interest rates have dropped, your credit score has improved, or you need lower monthly payments to ease cash flow.

Top up when you need urgent cash, your current loan terms are already good, and the extra funds will be used for income‑generating or essential purposes.

Applying for refinancing may cause a hard inquiry, which can temporarily lower your score. However, consistent repayment on the new loan will improve it over time.

Yes. This is called loan transfer or takeover. Kikwetu Sacco can pay off your external loan, and you repay us at lower rates.

Choosing between refinancing and a top‑up depends entirely on your goal.

Choose Refinancing if:

You want to save money, lower monthly payments, or get better loan terms. Refinancing is the long‑term winner.

Choose Top‑Up if:

You need quick cash, your current loan is already affordable, and you can handle higher payments.

Bottom line:

👉 Refinancing = saves you money.

👉 Top‑up = gives you more money (at a cost).

Link this article to your existing content:

Pillar page: SACCO Loan Top‑Up & Refinancing in Kenya (2026 Guide)

Related guides:

Membership pages:

Making the wrong loan choice can cost you thousands.

At Kikwetu Sacco, we help members compare options and choose what’s best for their situation.

👉 Talk to Kikwetu Sacco today and get expert guidance on:

Loan refinancing options

Loan top‑up eligibility

Affordable repayment plans

Take control of your finances now:

✔ Lower your monthly payments

✔ Access additional funds wisely

✔ Avoid financial stress

👉 Get started with Kikwetu Sacco now.

Last Updated: April 20, 2026

Reviewed by Kikwetu Sacco Financial Team

This content has been reviewed by the Kikwetu Sacco Financial Team, a group of professionals with experience in SACCO lending, savings management, and financial literacy in Kenya. The review ensures the information is accurate, practical, and aligned with current credit and loan practices.

Join us today and start growing your money the smart way.

Your funds are safely stored with Kikwetu Sacco.

We prioritize superior service in all our interactions.

Access loans at lower rates than traditional banking institutions.

As part of a shared-goal community, members benefit from collective support.

We emphasize savings discipline, especially for Kenyan youth.

Members can save and borrow to invest in land, up to three times their saved amount.